“Who We Are”: A Discussion of Corporate Integrity and our Mission to Increase Access to Affordable Energy, Which Thereby Enhances Human Flourishing, Society and the Environment

Since the founding of our first enterprise in 1990, Brigham Exploration Company, our mission has been to improve human beings’ access to the hydrocarbons that power our lives. It is by pursuing this mission that we fulfill our core responsibility to create value for our owners, the essence of our corporate integrity. We are proud of the role that we play in providing energy security throughout economic cycles and in bettering human lives, while also delivering differentiated social and environmental progress.

We have a long history of being good stewards of not only stockholder capital but also of the environments and communities in which we live and operate. Our core obligation is to our stockholders, and we recognize that maximizing value for our stockholders requires that we optimize the outcomes for our broader stakeholders, including our employees, as well as the communities and the environments in which we operate.

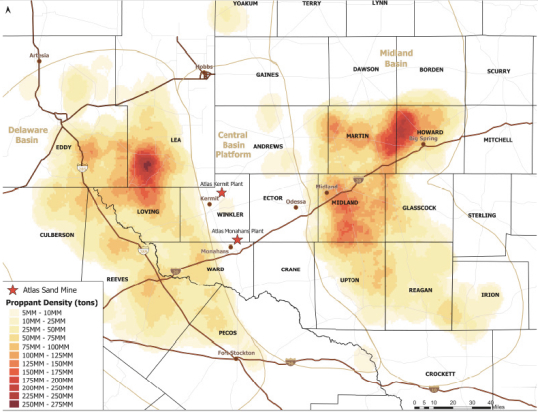

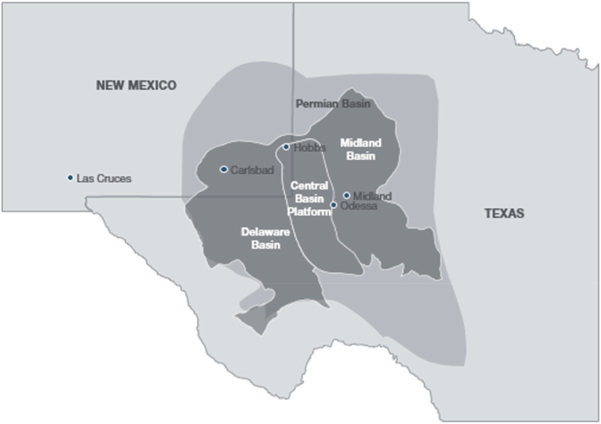

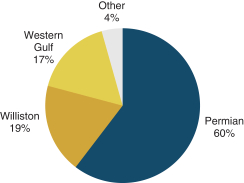

After leading Brigham Exploration, Brigham Resources Operating, LLC, and Brigham Minerals, Inc. through two successful initial public offerings and two substantial acquisition events, we recognized a compelling opportunity to capitalize on this track record and our experience by assembling the sand mining rights associated with approximately 38,000 acres in the Permian Basin—the most active basin in North America. So, we founded Atlas Energy in 2017, led by an experienced team of entrepreneurs from the oil and natural gas, transportation, industrial and proppant industries who have an established history of value creation and positive disruption in the energy industry. As a result, we designed and constructed our operations through the lens of an E&P operator benefitting from our history and roots in the energy industry, and we firmly believe that this orientation and mindset are reflected in our differentiated results. We have a relentless focus on the needs of our customers, and by creating value for them, we ultimately create value for our shareholders.

We are builders, innovators and, at times, constructive disruptors. Our success has stemmed from our ability to 1) generate leading-edge business ideas (leveraging our knowledge and experience), 2) hire great people, and 3) provide them with a collaborative and entrepreneurial environment. This approach has repeatedly created value for our owners, rewarding experiences for our employees, and attractive outcomes for our stakeholders, all while improving human beings’ access to the hydrocarbons that power our lives.

In order to attract and retain top-tier talent and to optimize their innovation and productivity, we create an entrepreneurial and collaborative work environment and provide our employees with compensation incentives (including equity) that align their interests with our owners. This approach enables us to deliver industry-leading innovation that drives down costs while elevating performance and has created value for our owners, rewarding experiences for our employees and attractive outcomes for our stakeholders.

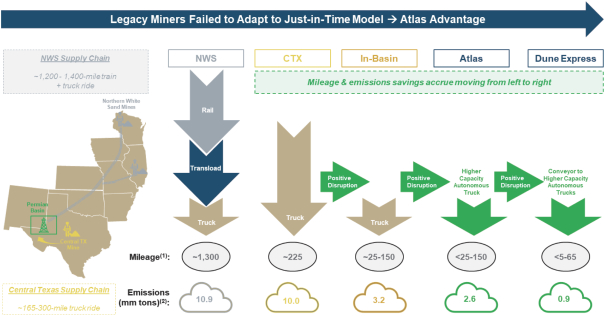

Our Atlas Energy team has driven innovation and has produced industry-leading environmental benefits by reducing energy consumption, emissions, and our aerial footprint. For example, our electrified dredging system, unique within the Permian Basin sand mining industry, reduces emissions by approximately 9.3 million pounds (4,230 metric tons) annually. The reputation for environmental

i